Most people first encounter the term “surety bond” the same way: a government application asks for one, a client requires proof of bonding, or a contractor license renewal pops up with a line item for a bond premium. What almost nobody explains clearly at that moment is what the bond actually does, who it actually protects, or what happens if something goes wrong. This guide covers all of it — the definition in plain language, the legal structure beneath it, the cost structure, the claim process, and the critical distinctions that determine whether bonding actually protects you.

The Surety Bond Definition

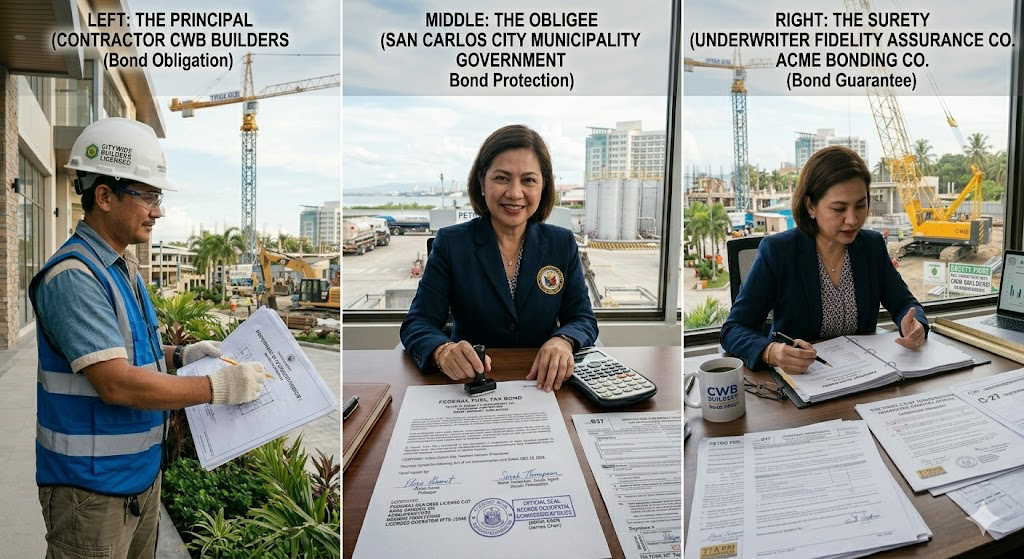

A surety bond is a legally binding, three-party written agreement in which one party — the surety — guarantees to a second party — the obligee — that a third party — the principal — will fulfill a specific obligation. That obligation may arise from a contract, a statute, a licensing requirement, or a court order.

The definition holds across all contexts: a surety bond is a promise backed by a financially rated third party that guarantees the performance, payment, or compliance of the party being bonded. If the principal fails, the obligee can file a claim. The surety investigates and, for valid claims, pays up to the bond’s full face value. The principal is then required by a separate agreement — the indemnity agreement — to reimburse the surety for every dollar paid, plus interest and fees.

The Cornell University Legal Information Institute, one of the most authoritative U.S. legal references, describes a surety bond as functioning like a security deposit that ensures legal or contractual duties are fulfilled. That analogy captures the essential mechanics: the money is there as a guarantee of performance, and whoever caused the failure is ultimately responsible for it.

The Three Parties, Defined

Every surety bond — regardless of industry, bond type, or dollar amount — involves these three parties:

| Party | Role | Financial Obligation |

|---|---|---|

| Principal | The business or individual being bonded | Pays the premium; must reimburse surety for all claims paid |

| Obligee | The government agency, project owner, or other party requiring the bond | Protected by the bond; files claims when the principal fails |

| Surety | The bonding company issuing the bond | Investigates and pays valid claims; recovers all payments from the principal |

These relationships form a triangle. The contract or regulatory requirement connects the obligee and the principal — it defines what the principal is obligated to do. The bond connects the obligee and the surety — it is the surety’s financial guarantee to the obligee. The indemnity agreement connects the surety and the principal — it is the contractual commitment that the principal will repay the surety for any claims paid on the principal’s behalf.

This triangular structure is what makes a surety bond fundamentally different from both a two-party insurance policy and a guarantee. Understanding the triangle is understanding the product.

Surety Bonds vs. Insurance: The Single Most Important Distinction

Every surety bond explanation in existence makes this point, yet businesses continue to confuse bonding with insurance coverage. The distinction matters practically, not just conceptually.

Insurance is a two-party risk transfer. The insured pays premiums into a risk pool, and when a covered loss occurs, the insurer pays — permanently. The insured does not repay the insurer. The insurance company prices premiums knowing it will pay claims. Losses are expected and built into the pricing.

A surety bond is a three-party guarantee, not a risk transfer. The surety does not absorb losses. The entire underwriting philosophy of the surety industry is built around issuing bonds only to principals believed unlikely to generate claims. Liberty Mutual states it plainly: surety is underwritten with the expectation that a claim is highly unlikely. When a claim is paid, the surety recovers it in full through the indemnity agreement. The principal ultimately pays for every dollar of every claim the surety issues.

The practical consequence: a bond does not protect the business owner. It protects the obligee — the government agency, project owner, or customer. Commercial insurance protects the business owner. In most licensed industries, both are required, and both serve entirely different financial functions.

What “Being Bonded” Actually Means

When a contractor, service provider, or professional advertises that they are “licensed, bonded, and insured,” the bond being referenced is typically a contractor license bond — not a performance bond or a payment bond covering the full value of a project. Contractor license bond amounts in most states range from $10,000 to $25,000. These amounts are set to protect against consumer losses from misconduct, not to guarantee completion of large construction contracts. A consumer who believes “bonded” means full project protection is often operating on a misconception the bond industry itself rarely corrects.

Being bonded, in its precise meaning, means you have purchased and filed a surety bond that guarantees a specific defined obligation — which could be compliance with a license, performance under a contract, faithful administration of an estate, or any of hundreds of other regulated obligations. The scope of what “bonded” means depends entirely on which bond was purchased and what its terms require.

The Penal Sum: The Bond’s Financial Ceiling

A key legal term in nearly every surety bond is the penal sum — the specified maximum dollar amount the surety can be required to pay in the event of the principal’s default. The penal sum is not the expected loss; it is the ceiling of the surety’s financial exposure. The premium charged by the surety is determined based on this penal sum, which is why sureties assess and price each bond type individually based on the obligations it covers.

Most modern US surety bonds set the penal sum at 100% of the underlying obligation — the full contract value for a performance bond, the full estate value for an executor bond, the full bond requirement for a license bond. The penal sum establishes the maximum, not the guaranteed payout.

The Indemnity Agreement: Why Surety Bonds Are Not Insurance

When a principal applies for a surety bond, they sign an indemnity agreement as part of the bond issuance process. This agreement is the mechanism that makes surety bonds legally distinct from insurance products. It contractually obligates the principal — and often personal indemnitors such as the business owner, spouse, and key principals — to reimburse the surety for all amounts paid on any claim, including legal fees and investigation costs.

If the surety pays a claim and the principal does not reimburse, the surety can pursue collection in court using the indemnity agreement as the basis for legal action. A signed indemnity agreement is enforceable as a contract. An unsatisfied surety indemnity obligation can result in civil judgments against the business, its owners, and any personal indemnitors who signed.

In most common-law jurisdictions, including all U.S. states, a contract of suretyship must be recorded in writing and signed by both the surety and the principal to be legally enforceable — a requirement rooted in the Statute of Frauds and its state equivalents.

Surety’s Right of Subrogation

One aspect of surety bonds almost never discussed in consumer-facing guides: the surety’s right of subrogation. When the surety pays a valid claim on the principal’s behalf, the law typically gives the surety the right to “step into the shoes” of the principal. This means the surety can pursue any third party who may also be liable for the loss — contractors, subcontractors, design professionals, or others whose actions contributed to the claim.

Subrogation gives the surety additional recovery avenues beyond simply chasing the principal under the indemnity agreement. It is a legally recognized right that arises automatically in most U.S. states even without an express agreement between the surety and principal. For large construction claims where multiple parties share liability, the surety’s subrogation rights can significantly affect how claims are ultimately resolved.

The Two Main Categories of Surety Bonds

All surety bonds divide into two broad categories:

Contract surety bonds are issued in connection with construction projects and guarantee that a contractor will perform according to the contract terms, pay all subcontractors and suppliers, and correct workmanship defects during the warranty period. Federal law requires contract surety bonds on any construction project valued at $150,000 or more. Most state and local governments have similar requirements under their own “Little Miller Acts.”

Commercial surety bonds cover everything outside of construction contracts — business licenses, court proceedings, public official positions, fiduciary appointments, and an enormous variety of regulated activities across every industry in the country.

Within these two categories, the industry recognizes five main subtypes of commercial bonds: license and permit bonds, court bonds (judicial and fiduciary/probate), public official bonds, fidelity bonds, and miscellaneous bonds.

How Surety Bond Costs Are Calculated

The bond premium — the actual cost paid by the principal — is calculated as a percentage of the penal sum (bond amount). The percentage depends on the principal’s credit profile, the bond type’s risk level, and the principal’s financial history and business track record.

| Credit & Risk Profile | Typical Premium Rate | Example: $50,000 Bond |

|---|---|---|

| Strong credit, standard bond | 0.5%–3% | $250–$1,500 per year |

| Fair credit | 3%–7% | $1,500–$3,500 per year |

| Poor credit or high-risk bond | 7%–15% | $3,500–$7,500 per year |

| Instant-issue, flat rate | ~1% | $500 per year |

A useful distinction Viking Bond Service makes explicit and most other guides conflate: the bond total (the penal sum — maximum payout) and the bond premium (what the principal actually pays — typically 1–5% of the total). These are not the same number. A $100,000 bond does not cost $100,000; it costs a premium of roughly $1,000–$5,000 annually depending on underwriting.

Premiums are paid on a bond term schedule — most bonds renew annually. As long as no claims are filed against the bond, the annual premium is the principal’s only out-of-pocket cost. A claim changes the economics entirely: the principal must repay whatever the surety pays, plus interest that compounds until the debt is settled.

The Claim Process Step by Step

When a claim is filed against a surety bond, the process follows a defined sequence that most general business guides skip entirely:

The claimant — the obligee or a harmed consumer — submits written documentation of the alleged violation to the surety, identifying the harm, the bond at issue, and the amount claimed. The surety opens a formal investigation. An impartial review determines whether the alleged conduct actually occurred, whether it falls within the scope of the bond’s coverage, and whether the claimed amount is accurate.

Invalid claims receive no settlement. Valid claims receive payment from the surety up to the penal sum. Following payment, the surety immediately turns to the principal under the indemnity agreement and demands reimbursement — the full amount paid, plus fees and interest that accumulates from the payment date forward. If the principal fails to pay, the surety pursues collection through the courts.

How to Get Your Surety Bond

The process begins by identifying the exact bond required. The obligee specifies the bond type, the required amount, and in many cases the bond form that must be used. Collect your business information, personal financial details, and credit history. Apply with a licensed surety producer — an agent or broker licensed to place surety bonds. Provide any required financial documentation. Receive a quote based on the underwriting review. Pay the premium, sign the indemnity agreement, receive your bond certificate, and file it with the obligee.

Swiftbonds processes surety bond applications for all bond types in all 50 states — from standard instant-issue license bonds to large-value construction performance and payment bonds that require complete financial underwriting packages. For businesses navigating a bond requirement for the first time, their team can confirm the exact bond form required, identify the correct bond amount, and file directly with the obligee once issued.

Swiftbonds LLC

Voted 2025 Surety Bond Agency of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

Frequently Asked Questions

What is the simplest way to explain what a surety bond does? A surety bond is a co-signed financial guarantee. The surety company co-signs the principal’s promise to perform, pay, or comply — and agrees to pay the obligee up to the bond’s full face value if the principal fails. The key detail most explanations omit: the principal must repay the surety every dollar paid on a claim. The surety’s payment is a temporary advance, not a permanent absorption of the loss.

Who does a surety bond protect — the business or the customer? The obligee and, where applicable, the consuming public. Not the business that purchased the bond. Commercial insurance protects the business owner. A surety bond protects the party requiring the bond — the government agency, project owner, client, or court. Both are needed for full risk management; they cover opposite sides of a business relationship.

What is the difference between a bond total and a bond premium? The bond total (penal sum) is the maximum the surety will pay on a claim — the financial ceiling of the bond. The bond premium is what the principal actually pays to the surety to maintain the bond, typically 1–5% of the bond total per year. A $50,000 bond does not cost $50,000; it costs a premium of roughly $500–$2,500 per year depending on credit.

What is a penal sum? The penal sum is the term used in surety law for the bond’s maximum payout amount. It is the dollar figure against which premiums are calculated and claims are measured. If a valid claim is filed, the surety pays up to the penal sum — not more, regardless of actual damages.

Is a surety bond the same as being insured? No. Surety bonds and insurance are structurally different products. Insurance is a two-party risk transfer where the insurer permanently absorbs covered losses. A surety bond is a three-party guarantee where the principal remains financially responsible for all losses — the surety is a temporary payer, not a permanent absorber. The practical result: a bond claim generates a debt owed by the principal to the surety; an insurance claim does not.

What does the Statute of Frauds have to do with surety bonds? In most common-law jurisdictions, including U.S. states, a suretyship agreement is only legally enforceable if it is in writing and signed by both the surety and the principal. This is a requirement under the Statute of Frauds — the legal doctrine that certain types of contracts must be written to be binding. Verbal surety agreements are generally unenforceable.

Can a surety bond claim be investigated and denied? Yes. Unlike letters of credit, which are pay-on-demand instruments, surety bonds are conditional — the surety has the right and obligation to investigate before paying. If the investigation finds the claim invalid, the surety denies it. The claimant can then pursue the matter through arbitration or court action. This conditional nature gives the principal a layer of protection against fraudulent or unsupported claims.

What is the surety’s right of subrogation? After paying a valid claim, the surety automatically acquires the legal right to “step into the shoes” of the principal and pursue any third parties who may also share responsibility for the loss that generated the claim. This right of subrogation allows the surety to seek recovery from sources beyond the principal’s indemnity obligation, such as other contractors, design professionals, or subcontractors whose actions contributed to the default.

What is an Electronic Surety Bond (ESB)? An Electronic Surety Bond is a digital version of a traditional paper surety bond. The Nationwide Multistate Licensing System and Registry (NMLS) initiated an ESB system starting in 2016, allowing certain bond types to be issued, tracked, and maintained digitally for licenses managed through NMLS. ESBs speed issuance, reduce paperwork, and enable direct electronic filing with regulatory agencies. The rollout has expanded state by state since 2016.

Conclusion

A surety bond is, at its core, a trust mechanism — a way to give parties who have never worked together a credible financial guarantee that the promises made at the start of a relationship will hold up under pressure. The definition is precise: three parties, one obligation, one financial guarantee, one unconditional reimbursement requirement. The product’s power comes from what that structure does to incentives: because the principal ultimately pays every dollar of every claim, principals who know they will be bonded have a strong financial reason to perform, comply, and pay. For business owners navigating bonding requirements for the first time, the operational priorities are clear — know which bond is required, understand that it protects your clients not you, and never let a bond lapse.

5 Surety Bond Definition Facts the Top 10 Sites Don’t Cover

1. A surety bond can protect a business from invalid claims in a way that a letter of credit cannot. Because surety bonds are conditional instruments — meaning the surety investigates before paying — the principal has an institutional advocate when a disputed or fraudulent claim is filed. If an obligee files a bad-faith claim against a surety bond, the surety’s claims department investigates, finds the claim invalid, and denies it. If the same obligation were backed by a letter of credit, the bank pays the moment the obligee makes a demand, with almost no investigation or defense. For principals with legitimate disputes, the surety bond’s conditional structure is a meaningful protection that no guide covering the basic “what is a surety bond” question discusses.

2. Surety bond premiums paid as a required cost of operating a licensed business are generally deductible as ordinary and necessary business expenses under IRS Section 162. For businesses renewing contractor license bonds, freight broker bonds, mortgage broker bonds, or any other bond required as a licensing prerequisite, the annual premium is a deductible operating cost — in the same category as state license fees and regulatory compliance expenses. For large businesses maintaining multiple bonds or high-dollar construction bonds, this deduction can add up to a meaningful annual figure. Every surety bond guide explains what bonds cost; none of the top 10 pages on this keyword explain that businesses can deduct those costs.

3. The “bonded and insured” phrase used in contractor marketing is widely misleading to consumers. When a home services contractor lists “fully licensed, bonded, and insured” on their truck or website, the bond is almost always a contractor license bond — a small-dollar compliance instrument with a face value of $10,000–$25,000 in most states. This bond does not cover the cost of completing a failed or abandoned project worth $80,000. Consumers who believe “bonded” provides comprehensive protection against nonperformance are operating on an industry-wide misconception that the surety bond industry has no structural incentive to correct. Understanding the difference between a license bond and a performance bond is the single most consumer-protective piece of knowledge in the entire surety education landscape.

4. The surety industry’s 14.5% direct loss ratio (2022) is one of the lowest of any financial services product in the United States. SFAA 2022 preliminary data shows the US and Canadian surety market produced $8.6 billion in direct written premium with a 14.5% direct loss ratio. This extraordinary low-loss performance is not because sureties are lucky — it is because the entire product is designed around pre-loss qualification. Sureties only bond principals they believe will perform without a claim. The result is a product that provides real financial protection to obligees while almost never actually paying — which is precisely the point. No insurance product achieves anything close to a 14.5% loss ratio while maintaining meaningful coverage.

5. The penal bond — the historical predecessor of the modern surety bond — operated with only two parties, not three. Medieval and early modern penal bonds were two-party instruments: an obligor (debtor) and an obligee (creditor). The obligor would sign a bond acknowledging a debt of double or triple the principal amount, with a condition attached that nullified the bond if the underlying obligation was performed. The modern three-party surety bond — with a separate surety guaranteeing the principal’s performance — emerged as the dominant form precisely because two-party penal bonds relied entirely on the obligor’s solvency. Adding the surety as a creditworthy guarantor solved the fundamental limitation of the penal bond and gave birth to the modern bonding industry.

Leave a Reply